[ad_1]

Having appeared on the qualitative rationale for why options-based funds are provided by fund managers and sought by some traders, it behooves us to quantitatively analyze choices funds’ efficiency. There isn’t any ONE BENCHMARK that can be utilized to check ALL the choices funds. That could be a superb factor. It’s made me consider what a great way to create a personalized benchmark for every fund may appear to be. The good thing about conserving issues centered on the small image is we are able to have a look at one fund at a time, intimately, with out drawing too many generalizations.

Challenges with choice fund efficiency comparisons

The vast majority of choice funds have solely been round for just a few years. This creates challenges in evaluating their efficiency. For instance:

- It’s not attainable to run 10, 20, or 30-year analyses on a big sufficient pattern of those funds and we can’t consider the funds as an Asset class.

- Variety throughout the options-based funds makes it tough to check any 2 funds. One of many targets of the accompanying article was to level out the various kinds of Fairness sleeves and the differing decisions made by fund managers. We are able to’t evaluate Giant-cap Tech shares to small-call Worldwide worth shares any greater than we are able to evaluate choice revenue/premium funds to hedged fairness funds. Add the funky new class of funds that carry only one inventory and overwrite each day or weekly choices. There’s NO PEER group right here. Peer Averages imply nothing.

- The final main 50% fairness market crash was in 2007-2009. Most of those funds didn’t exist in that crash or the 2000-2002 50% crash. We don’t understand how these funds will carry out within the subsequent main crash. (PS: There’ll all the time be a subsequent main crash regardless of how good every little thing seems to be in the intervening time).

- The significance of observing lively choice portfolios by a inventory market crash (even bearish portfolios) is to learn the way the fund supervisor offers with coincident issues of illiquidity, excessive transaction prices, and volatility to get out and in of shares and choices. Spinoff markets want deep liquidity in underlying shares. In crashes, when this liquidity disappears, spinoff market makers merely stroll away or present absurd costs. How will that have an effect on choices funds? We don’t know but.

- When funds have a younger age, their efficiency information are dictated by the timing of the launch and never essentially the long-term benefit of a method. There isn’t any must get too enthusiastic about each new choices technique. Energetic fairness choosing, excessive charges, and the burden of buying and selling a lot of spinoff contracts all add up as prices. Choices exchanges and choices market makers are raking in tons of income. Who’s paying for it? Don’t go searching. It’s all the cash going into Zero Day choices and choices funds.

Challenges with choice fund efficiency comparisons: the S&P 500 is an unbeatable index

When I’m launched to any new US Fairness linked fund, my first intuition is to check it to the S&P 500. Is the fund distinctive in any means that may assist my portfolio develop?

Evaluating fairness choices funds to the S&P 500 (or the Nasdaq 100 the place relevant) yields predictably disappointing whole outcomes.

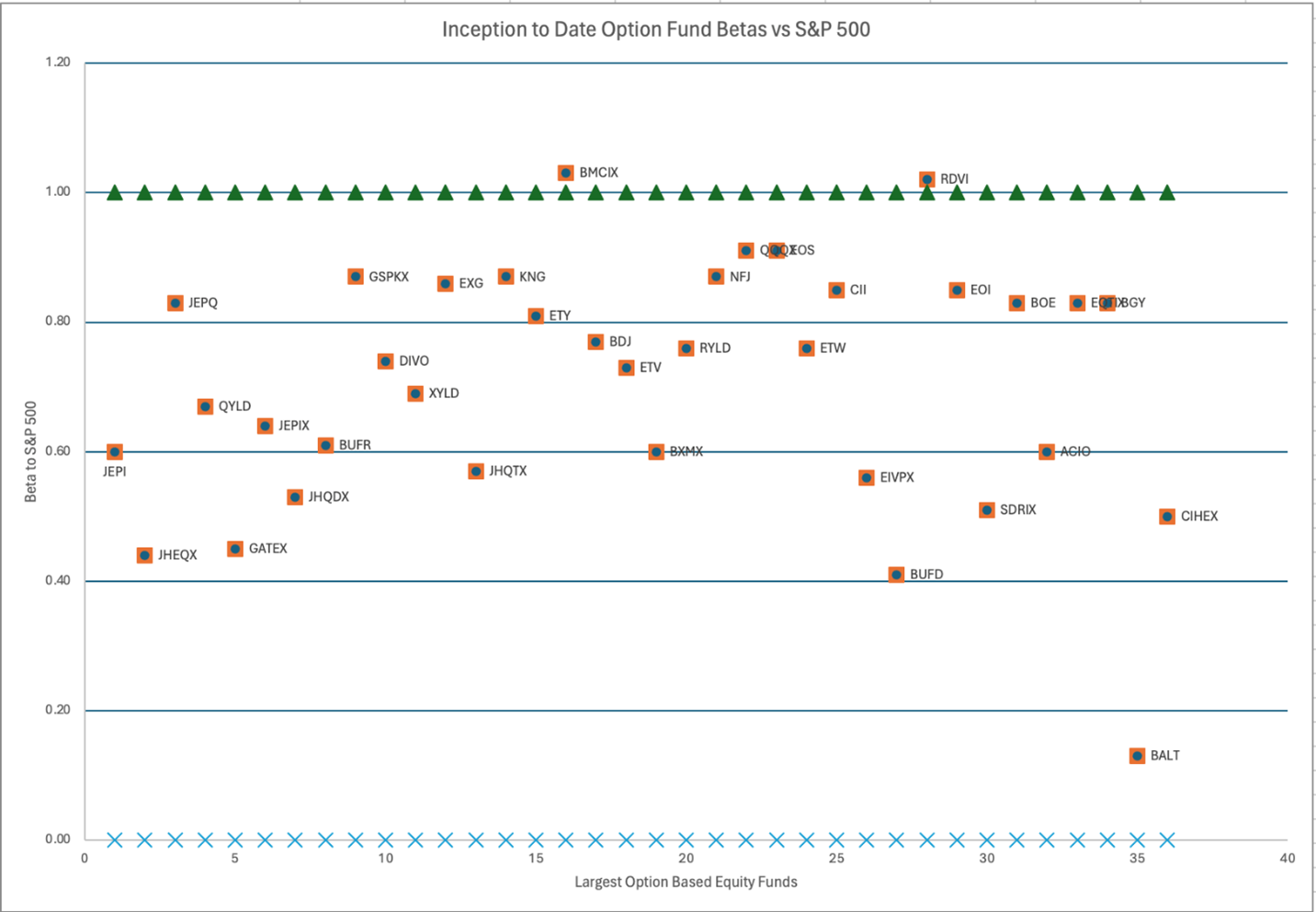

To know why, we should deal with Fund Betas.

The S&P 500, that’s, the market in US equities, by definition has a Market Beta of 1.

The Betas of most of those choices funds (orange squares within the chart) are decrease than 1 (the S&P 500 marked by the Inexperienced mountain vary).

Since US fairness markets have gone up over time, a decrease beta = decrease market publicity = decrease whole returns.

It’s essential to seize the right window for calculating returns. I’ve tried to do this under.

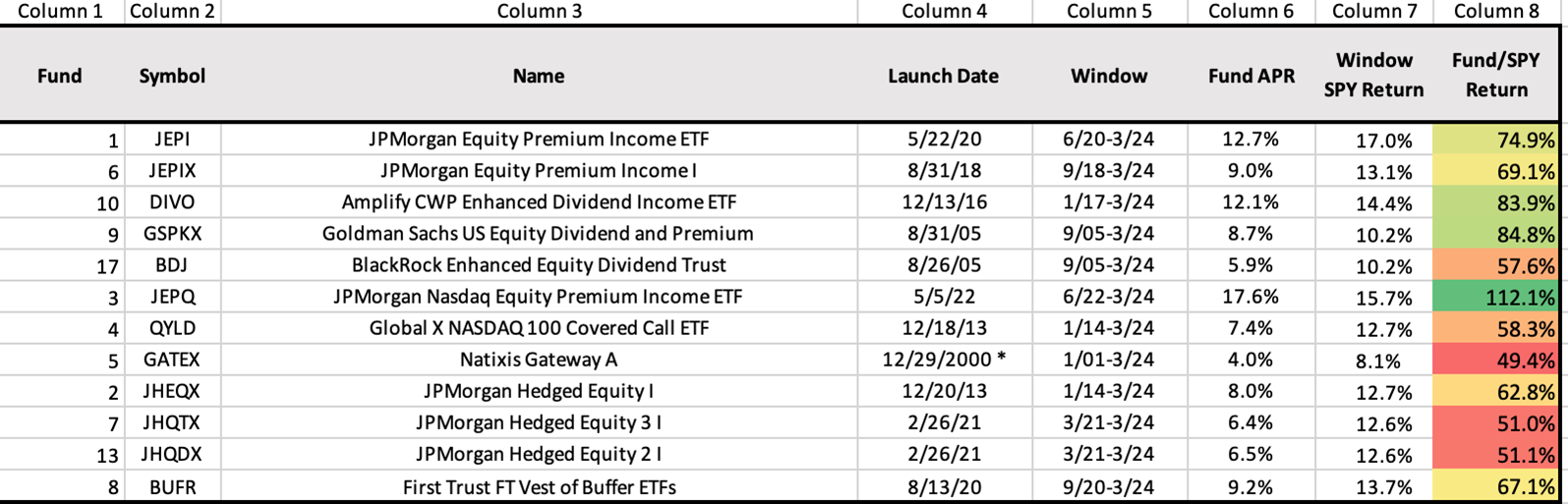

Utilizing the slender listing of funds we qualitatively described within the accompanying article, I present every fund’s launch date (Column 4) and the analysis window (Column 5). Then, in Column 6, I have a look at the Annualized return of the fund since that date and evaluate it to the Annualized Return of SPY in that window (Column 7).

Evaluating Columns 6 and seven ought to level out that different one fund, JPMorgan Nasdaq Fairness Premium Revenue (JEPQ), no different massive choices fund beat the straightforward passive SPY. What a bummer!

Column 8 compares the Fund’s annualized returns to the SPY’s to indicate what % of the SPY the fund earned.

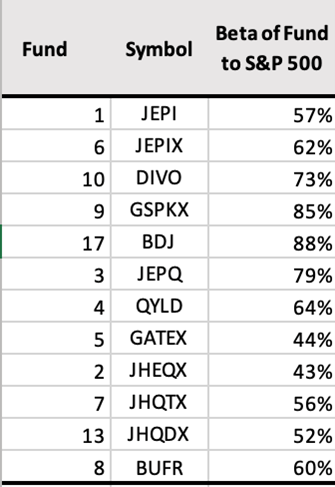

Desk 1

On common, this small number of funds largely underperformed SPY.

(Fund #3) JEPQ earned 112.1% of SPY whereas (Fund #5) GATEX earned solely 49.4% of the SPY.

Why did JEPQ earn a living? As a result of the Fairness sleeve is the Nasdaq 100 sort names. Nasdaq beat the S&P massively for the reason that 2009 bull market began.

Nevertheless, QYLD didn’t succeed. Why? Cause #1, whereas JEPQ sells out-of-the-money calls on the Nasdaq to earn Revenue, QYLD sells At-the-money calls. In an index going straight up, how we use choices issues. Cause #2, QYLD has been round since 2013 whereas JEPQ is youthful. It’s one other lesson to attend and decelerate. New funds have a timing good luck/dangerous luck issue.

Take a more true comparability. For JEPQ and QYLD, let’s use QQQ as an alternative of SPY and we get this:

Desk 2

JEPQ now not seems to be like a star and QYLD seems to be like a complete dud.

In any case, this evaluation in incomplete. Wanting solely on the Complete Return does a disservice to the choices funds. There are different metrics just like the fund’s relative St. Dev to the SPY, Betas, or the Sharpe ratios, the worst drawdowns, and so forth. Let’s take a type of metrics and stretch our evaluation.

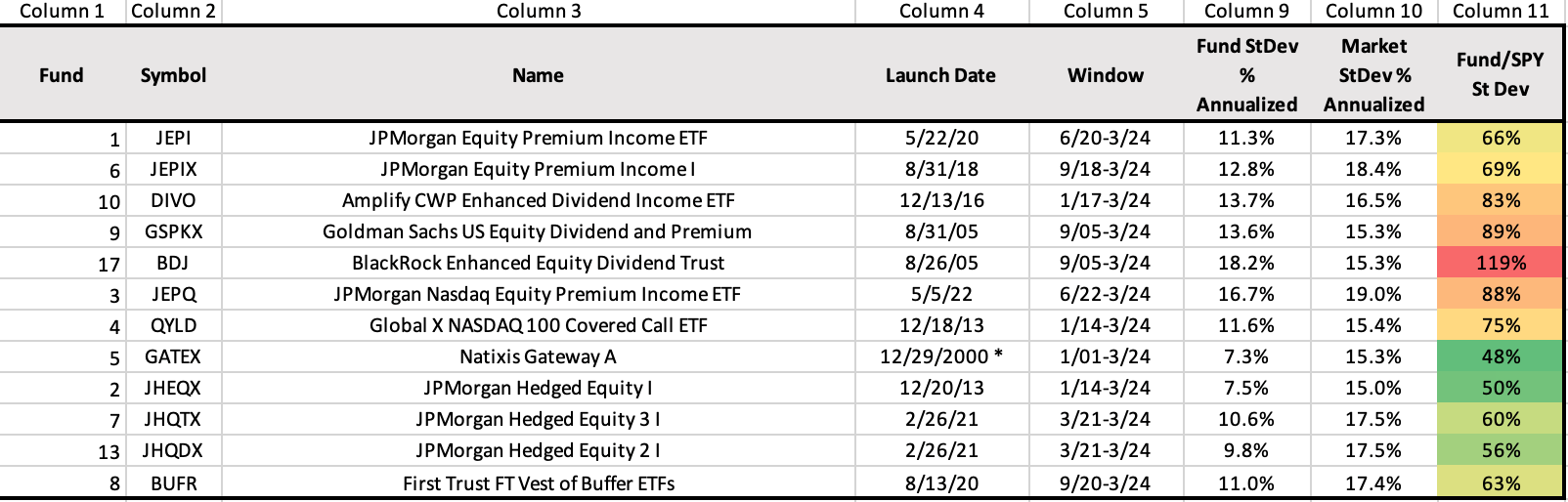

Comparability to the S&P 500: Customary deviation issues

Traders’ expectation is just not that choices funds would earn greater returns. Fairly, traders hope the funds will exhibit decrease volatility and make the journey smoother. The traders hoped to nonetheless earn a number of the fairness returns with decrease volatility than the market.

Desk 3

The truth is, that’s very a lot the case. Within the above desk, calculated utilizing Portfolio Visualized, I’ve highlighted our small group of funds, this time, in Columns 9 and 10, I’ve offered how risky the fund has been in the course of the window on an annualized foundation versus the volatility of the Market. We’ve used % Annualized Customary Deviation as a measure. In Column 11, we present the St. Dev of the fund as a % of the SPY.

We are able to see that each one besides (Fund #17) BDJ had a decrease commonplace deviation than the SPY with the triplets of JHEQX/JHQTX/JHQDX (Fund 2, 7, 13) exhibiting the bottom Std. Deviation in comparison with the SPY.

BUFR (Fund 8) is just not far behind.

These funds are widespread in that these final 5 funds in that desk are “Hedged”, “Protected”, or “Buffered” and intend to offer draw back safety. Those above are usually Revenue suppliers and supply no draw back safety.

In layman’s phrases, this can be a vindication of the fund managers’ commercial pitch and the investor’s hopes: Decrease returns accompanied with decrease volatility.

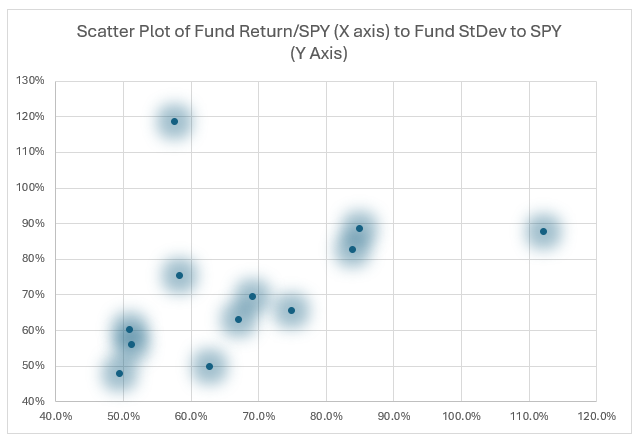

Combining the 2 tables above, I’ve plotted the Return % of those funds and the Std Dev of those funds in comparison with the SPY. In brief, returns between 50-90% with a volatility of 50-90% of the SPY.

Chart 1

Making a replicating portfolio to push our evaluation even additional:

Why ought to we permit choices funds a straightforward go? In monetary markets, there are a number of method to get to the identical finish level. We now know that choices funds have a decrease Beta to the S&P 500 (as calculated by Portfolio Visualizer)

Desk 4

Let’s take only one fund, JEPIX, which is the Mutual Fund equal to JEPI. Collectively they maintain a mixed $39 Billion in property. Utilizing Portfolio Visualizer, I checked the Beta of JEPIX for every calendar yr since its inception in Fall of 2018.

Desk 5

JEPIX Betas change dramatically from yr to yr and appear to be on a downward development just lately.

Why does the Beta transfer a lot yr to yr? It may very well be the Fairness Sleeve and which shares go within the portfolio. Maybe the fund managers have a decrease volatility portfolio of shares in 2024 in comparison with 2013. It is also the interplay of the choices used with the Fairness Portfolio and their mixed impact.

It doesn’t matter. These funds are always altering their underlying traits as a result of they’re Actively managed. We are able to’t inform what the Fund supervisor is pondering. What we CAN DO is inform what the historic Betas have been.

Within the case of JEPIX, the story is that this Fund has a lifetime of 0.62 to the S&P 500 Index.

Proposal: Create a Replicating Portfolio

We all know that the beta of the S&P 500 (which stands for the market index within the USA) is 1 and we all know the Beta of T-Payments is 0. T-Payments have zero beta as a result of these below 1-year Authorities devices don’t have anything to do with the Inventory Market. They’re short-term obligations of the US Authorities issued by the Division of Treasury to fund the Authorities.

We are able to mix a easy 2 fund portfolio of SPY and T-Payments with the ratio of 61% SPY and 39% BIL (the T-Invoice ETF). They received’t have a Beta precisely of 0.62 (in actual fact, in accordance with Portfolio Visualizer), the 2-fund Replicating Portfolio has a Beta of 0.59 throughout our Replicating window of Sep 2018 to March 2024. That’s advantageous. We’re capturing for simplicity.

Moreover, we are able to select an choice for Annual Rebalancing in portfolio visualizer so the SPY+BIL portfolio rebalances to 62% SPY each calendar yr. (If we don’t try this, SPY will hold changing into a much bigger % of the portfolio. We wish to match the approximate Beta of JEPIX on common over its life).

I ran that easy 2-fund portfolio in Portfolio Visualizer alongside JEPIX. Charts and statistics:

Chart 2

Do you see the distinction between the blue line JEPIX and the pink line, Replicating portfolio?

NO? As a result of there isn’t any. The 2 charts look nearly the identical. Possibly just a little extra return in some durations and provides again in others, however the variations are minuscule.

Desk 6

$100 invested in JEPIX and the 2-fund portfolio could be equal nearly the identical 5 ¼ years since launch.

For some traders, it may not matter that JEPIX isn’t any higher than a easy 62/38 SPY/BIL portfolio. That it’s earned 9% annualized is sweet sufficient. My objective is to not get traders to purchase or not purchase a fund. It’s to assist simplify and demystify a fund.

Our evaluation brings us as near residence as we are able to count on to be. If we are able to take all of the magic supplied by all of the monetary merchandise and simplify it so we are able to perceive how we are able to reconstruct that magic ourselves, then we’d really feel just a little extra assured in our decision-making course of.

Let’s take a case the place the outcomes are NOT equal: GATEX

Step 1: Decide a window to calculate Beta. Let’s go along with 7 years

Desk 7

Step 2: Equal Portfolio = 46% SPY 54% T-Invoice for interval 2018 to 2024 March. Select Annual Rebalancing in Portfolio Visualizer

Step 3: Output 1: Chart3

Output 2: Metrics: Desk 8

GATEX underperforms the Replicating Portfolio by 2.77% per yr with the next Customary Deviation than the Replication.

By all metrics, GATEX can’t beat a passive replicating portfolio. It has a bigger max drawdown and a worse Sharpe Ratio.

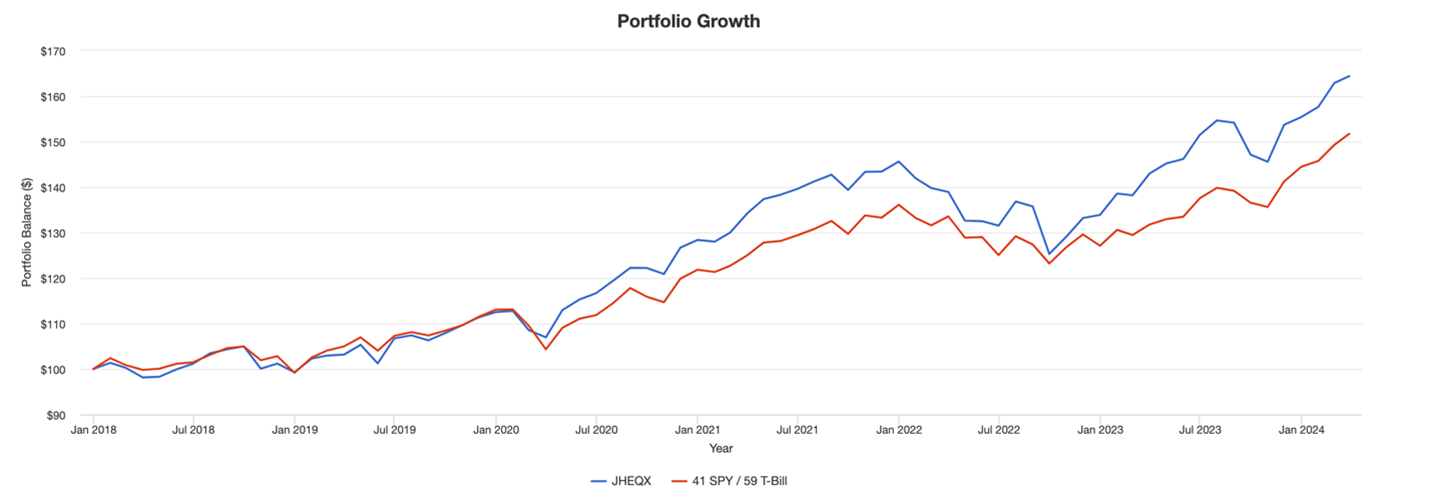

Let’s take a case the place the choices fund works properly: JPMorgan Hedged Fairness Fund (JHEQX).

Step 1: Decide a window to calculate Beta. Let’s go along with 7 years

Desk 9

Step 2: Equal Portfolio = 41% SPY 59% T-Invoice for interval 2018 to 2024 March. Select Annual Rebalancing in Portfolio Visualizer

Step 3: Output 1: Chart 4

Output 2: Metrics

Desk 10

JHEQX had the next annualized return of 1.4% over the past 7 years than its Replicating Portfolio, albeit additionally barely greater commonplace deviation.

JHEQX is an efficient instance of an choice fund that has up to now labored.

Correct analysis is difficult work

We solely studied a small variety of the over 300 funds devoted to this house, evaluated a good smaller quantity, and so we don’t wish to make an excessive amount of out of our evaluation.

Analysis requires some work for every fund. It’s not plug-and-play as a result of the Replication portfolio for every fund must first be decided based mostly on the previous Beta of the choices fund.

We want a historical past for every fund. We are able to’t do that evaluation for a brand new fund till we’ve seen its beta versus the S&P.

Since I can’t do that for 300 choices funds, (and new funds are beginning on daily basis), my objective was to set a framework that others can construct on.

Let’s discuss concerning the fund that appears first rate: JPMorgan Hedged Fairness Fund (JHEQX)

JHEQX is a low-beta fund. On the 0.41 beta, it did a superb job outperforming the equal SPY and T-Invoice portfolio. An fascinating follow-up right here could be the newer JHQTX and JHQDX, designed in the identical vein as JHEQX. As Chart 5 under reveals, the Replicating Portfolio’s Orange line beat them each. Possibly the funds want extra time? Each time we expect choices funds may outperform, we peel the onion, and the proof requires extra time or extra evaluation.

Chart 5

The Fairness Sleeve

Earlier than we conclude, I wish to level out that selecting the right Fairness Sleeve is essential. An extended Nasdaq fairness sleeve was so highly effective over the past 10-years that it washed away any crimes dedicated on the choices legs.

Alternatively, selecting EM or Developed Market Passive Fairness sleeve may have been a horrible selection. No quantity of choices cleverness would have dissolved the crime of being invested in a passive EM ETF.

Coming to an finish: There’s a purpose why individuals purchase/maintain these funds

We took a disparate group of options-based funds and united them. We confirmed that Complete Returns and commonplace deviation needed to be checked out in sync and we completed this by the fund’s historic betas, created replicating portfolios, and used the fund’s return collection to check to the replicating portfolios. Our outcomes are essential as a result of they’re grounded in simplicity, and anybody can replicate the outcomes. Anybody can decide if “their” fund holds water.

Whereas analyzing quantitatively is essential, we should always bear in mind individuals purchase these funds for at the very least just a few completely different causes:

- Their brokers/advisors promote them the funds

- Traders usually are not enthusiastic about creating low-beta portfolios and rebalancing

- Incomes revenue was once essential in a zero-rate world. Choices funds had a spot. With T-Payments at 5.25%, possibly the choices for Revenue funds have to be rethought. However as soon as invested, the inertia to take cash out is nice. Funding merchandise are sticky.

- Tax payments are all the time a hindrance.

If we go to David Snowball’s thesis, “30% Fairness Allocation will get you a majority of the inventory market’s returns however skip a lot of the volatility”, we are able to admire the fantastic thing about low-beta portfolios (the success of JHEQX). Some choices Funds promise and ship the low beta portfolios. Some funds do it higher than others (= GATEX) and it’s our job as finish traders to choose the nice ones and ignore the poor ones.

Whereas options-based funds maintain no magic bullets, and a majority of their returns may be replicated by easy SPY+T-Invoice portfolios, there’ll all the time be a requirement for choices funds. For so long as traders have been invested in dangerous property, they’ve needed a smoother journey.

[ad_2]