[ad_1]

Firm overview

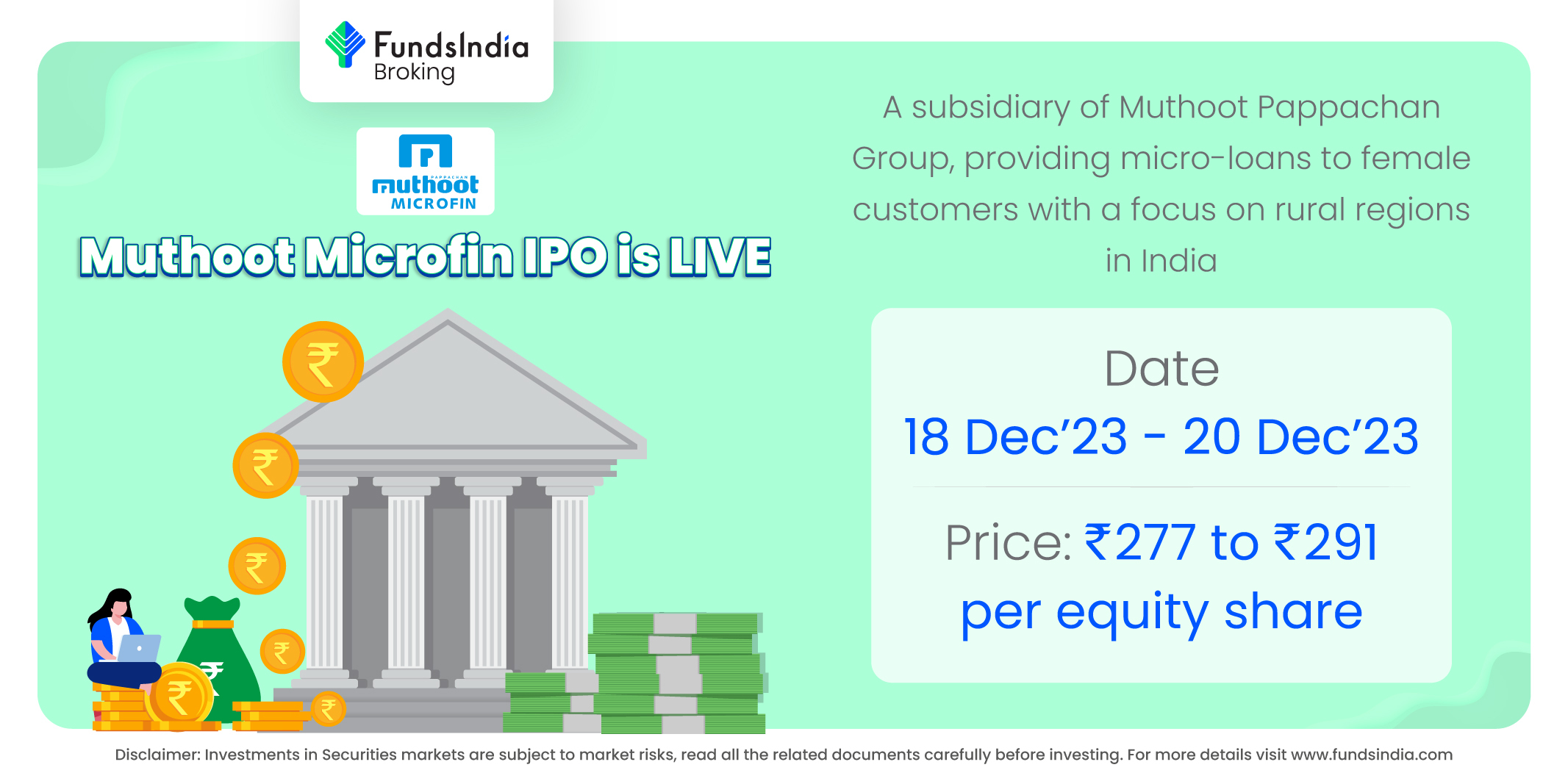

Muthoot Microfin Ltd is Non-Banking Monetary Firm-Micro Finance Establishment (NBFC-MFI) offering microloans to girls clients (primarily for revenue technology functions) with a deal with rural areas of India. The corporate is part of Muthoot Pappachan Group, a enterprise conglomerate with a historical past of over 50 years in monetary providers enterprise. It’s the second largest firm underneath the Muthoot Pappachan Group, by way of AUM for the Monetary 12 months 2023. As of March 31, 2023, the corporate has 2.77 million lively clients, who’re serviced by 10,227 workers throughout 1,172 branches in 321 districts in 18 states and union territories in India.

Objects of the provide

- Augmenting the corporate’s capital base to satisfy future capital necessities.

- To undertake present enterprise actions.

- To undertake the actions proposed to be funded from the Internet Proceeds.

- Obtain the advantages of itemizing Fairness Shares on the Inventory Exchanges.

- Perform provide on the market of as much as 6,872,852 Fairness Shares by the Promoting Shareholders

Funding Rationale

- Diversified product portfolio – The corporate primarily present loans for revenue producing functions to girls clients dwelling in rural areas. The mortgage merchandise comprise (i) group loans for livelihood options resembling revenue producing loans, Pragathi loans (that are interim loans made to present clients for working capital and revenue producing actions) and particular person loans; (ii) life betterment options together with cell phones loans, photo voltaic lighting product loans and family home equipment product loans; (iii) well being and hygiene loans resembling sanitation enchancment loans; and (iv) secured loans within the type of gold loans and Muthoot Small & Rising Enterprise (“MSGB”) loans. In 2021, the corporate launched its proprietary software “Mahila Mitra”, paving manner for digital assortment infrastructure which facilitates digital fee strategies resembling QR codes, web sites, SMS-based hyperlinks and voice-based fee strategies. Collaborating with M-Swasth since December 2021, the corporate provides digital healthcare services to its clients by e-clinics. Moreover, it additionally gives pure calamity insurance coverage merchandise to its clients.

- Market management with pan India presence – As of March 31, 2023 the corporate’s gross mortgage portfolio amounted to Rs. 9208 crores. 95% of this was comprised of revenue producing loans totaling Rs. 8746 crores. It’s the fourth largest NBFC-MFI in India by way of gross mortgage portfolio as of December 31, 2022. It’s also the third largest amongst NBFC-MFIs in South India by way of gross mortgage portfolio, the most important in Kerala by way of MFI market share, and a key participant in Tamil Nadu with an nearly 16% market share, as of December 31, 2022. The corporate’s strong danger administration framework, buyer choice methodologies and common finish use and fee monitoring have resulted in wholesome portfolio high quality indicators resembling excessive assortment effectivity, secure PAR and low charges of gross NPAs and internet NPAs. Assortment effectivity was 95.84% for the Monetary 12 months 2023, and gross NPA ratio was 2.97% and internet NPA ratio was 0.60%, as of March 31, 2023. As of December 31, 2022, the corporate had the second lowest gross NPA ratio and internet NPA ratio among the many chosen NBFC-MFIs.

- Monetary Monitor Document – The corporate reported a income of Rs.1429 crores in FY23 as towards Rs.833 crores in FY22, a rise of 72% YoY. The income has grown at a CAGR of 45% between FY2021-23. The corporate posted curiosity revenue of Rs.1291 crores in FY23 as towards Rs.729 crores in FY22, a rise of 77% YoY and a CAGR of 44% between FY21-23. The EBITDA of the corporate in FY23 was Rs.788 crores and EBITDA margin was at 55%. The PAT of the corporate in FY23 is at Rs. 164 crores and PAT margin is at 11%. The CAGR between FY2021-23 of EBITDA is 55% and PAT is 384%. The ROE of the corporate stands at 11% in FY23. GNPA improved from 6.26% in FY22 to 2.97% in FY23. NNPA improved from 1.55% for FY22 to 0.60% for FY23.

Key dangers

- OFS danger – Along with recent difficulty, the IPO will see the provide on the market of shares value upto Rs.70 crores every by promoters Thomas John Muthoot, Thomas Muthoot and Thomas George Muthoot, Rs. 30 crores every by promoters Preethi John Muthoot, Remmy Thomas and Nina George, and Rs.100 crores by investor Larger Pacific Capital WIV Ltd.

- Regulatory danger – As an MFI, the corporate is topic to inspections by RBI. Non-compliance with observations made by the RBI throughout these inspections may expose the corporate to penalties and restrictions which could have a fabric impression on the enterprise and working efficiency.

- Default danger – The danger of non-payment or default by clients could adversely have an effect on the corporate’s enterprise, outcomes of operations and monetary circumstances. The corporate’s goal buyer phase is predominantly girls from rural areas who usually has restricted sources of revenue, financial savings and credit score histories which could have an effect on the credit score worthiness and compensation capabilities.

Outlook

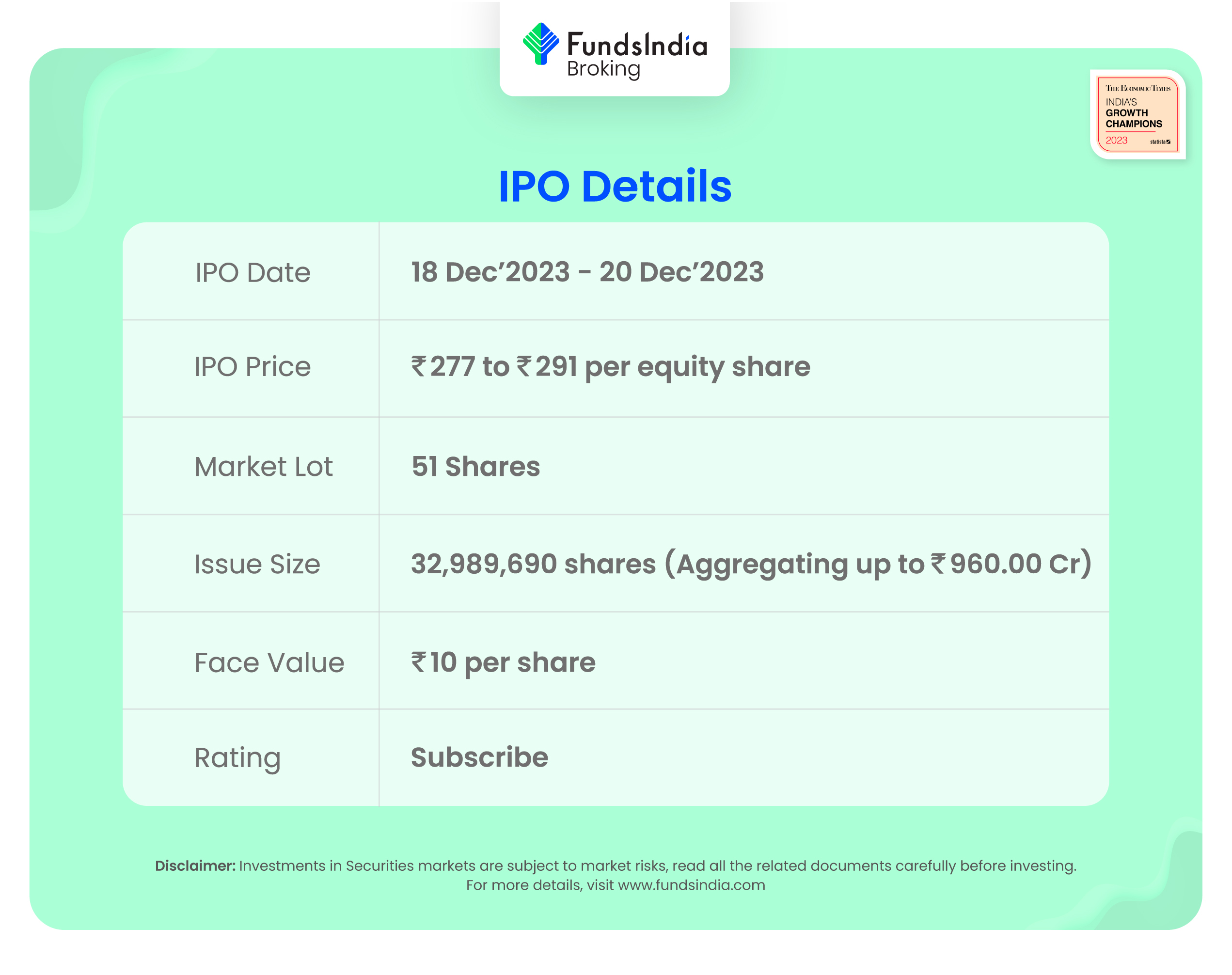

With the corporate’s operations concentrated traditionally in South India, the corporate has not too long ago began to broaden into North, West and East India and have a complete of 596 branches throughout North, West and East India as of March 31, 2023, representing 50.85% of whole branches as of March 31, 2023. The corporate’s technique of growth throughout numerous geographies in India and rising buyer base is anticipated to help the corporate to proceed its ongoing progress for future years as effectively. In keeping with RHP, Equitas Small Finance Financial institution Restricted, Ujjivan Small Finance Financial institution Restricted, CreditAccess Grameen Restricted and Suryoday Small Finance Financial institution Restricted are few of the listed opponents for Muthoot Microfin. The friends are buying and selling at a median P/E of 18.22x with the very best P/E of 26.67x and the bottom being 6.33x. On the increased worth band, the itemizing market cap of Muthoot Microfin can be round ~Rs.4159.96 crores and the corporate is demanding a P/E a number of of 25.23x primarily based on submit difficulty diluted FY23 EPS of Rs.11.54. Compared with its friends, the difficulty appears to be absolutely priced in (pretty valued). Based mostly on the above views, we offer a ‘Subscribe’ score for this IPO for a medium to long-term Holding.

If you’re new to FundsIndia, open your FREE funding account with us and luxuriate in lifelong research-backed funding steering.

Different articles you could like

Submit Views:

59

[ad_2]