{kind=link}

Over the previous 12 months and alter, mortgage refinance functions have fallen off a cliff.

We had among the greatest refi years in 2020 and 2021, adopted by the worst 12 months for mortgage functions this century.

And it’s all as a result of mortgage charges hit all-time lows, then abruptly surged to round 8% in simply over 12 months.

Charges on the 30-year mounted have since settled in round 7%, and there’s hope they’ll proceed to drop into 2024.

If that’s the case, we would see a return to price and time period refinancing as current residence consumers search out cost aid.

Does Anybody Refinance Their Mortgage Anymore?

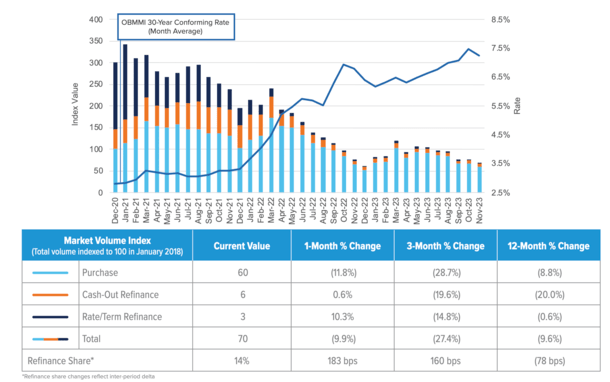

As famous, mortgage refinancing hasn’t been very talked-about in 2023. After a number of banner years, the low-rate mortgage occasion got here to an finish.

In any case, most owners already took benefit when charges have been low. And only a few are forgoing their 2-4% mortgage price to faucet into their residence fairness.

As an alternative, they’re choosing a second mortgage in the event that they want cash, comparable to a residence fairness mortgage or HELOC.

This permits them to retain their low-rate first mortgage whereas nonetheless accessing their fairness.

However as a result of mortgage charges have hovered within the 6-8% vary for a lot of the previous 12 months, and charges have since improved a bit, the refi functions are starting to trickle in.

Per the newest Originations Market Monitor report from Optimum Blue, the 30-year mounted improved by 67 foundation factors throughout the month of November.

For some lenders, we’re speaking a price drop from round 8% to 7%. This resulted in a ten% month-over-month enhance in price and time period refinance functions.

If charges proceed to maneuver decrease, we would see apps rise much more in 2024.

And since many current mortgage holders have very excessive charges, cost aid will really be simpler to return by. Enable me as an instance.

Refinancing an 8% Mortgage Fee to a 7% Fee

$500k mortgage quantity @8% = $3,668.82

$500k mortgage quantity @7% = $3,326.51

Month-to-month financial savings: $342

Let’s think about a current residence purchaser bought a property when mortgage charges peaked at round 8%.

We’ll faux they bought a house for roughly $556,000 with a ten% down cost, leaving them with a $500,000 mortgage quantity.

This could end in a month-to-month principal and curiosity cost of $3,668.82, assuming it was a 30-year mounted mortgage.

Now in the event that they have been to refinance to a 7% price, the month-to-month P&I’d drop to $3,326.51. That’s a $342 discount in month-to-month cost.

Not too shabby, proper? Certain, the speed continues to be a far cry from the three% mortgage charges on provide in 2021, however the financial savings are strong.

Refinancing a 5% Mortgage Fee to a 4% Fee

$500k mortgage quantity @5% = $2,684.11

$500k mortgage quantity @4% = $2,387.08

Month-to-month financial savings: $297

Think about the identical mortgage state of affairs, however with a 5% mortgage price. That places the month-to-month P&I at $2,684.11.

That’s about $1,000 decrease every month than the 8% mortgage price, which explains the affordability disaster presently happening.

Once more, let’s faux mortgage charges fall by one proportion level and the home-owner seems to be right into a refinance.

If they may change their 5% price for a 4% price, they’d see a month-to-month cost of $2,387.08.

That’s solely $297 in financial savings in every month, about $45 lower than the home-owner who refinanced from 8% to 7%.

In different phrases, the borrower who refinanced from one excessive price to a barely decrease excessive price saved extra.

Refinancing an 8% Mortgage Fee to a 6% Fee

$500k mortgage quantity @8% = $3,668.82

$500k mortgage quantity @6% = $2,997.75

Month-to-month financial savings: $671

Now let’s assume mortgage charges proceed to fall all through 2024 and hit 6%. That is really consistent with some 2024 mortgage price predictions.

Once more, we’ll use our 8% mortgage price borrower and their $500,000 mortgage quantity as an instance.

They’d see their month-to-month P&I fall to $2,997.75, which might signify about $671 in month-to-month financial savings.

That’s a reasonably large win for somebody seeking to scale back their month-to-month housing expense. I can’t consider many different methods to decrease your prices.

That is that date the speed, marry the home argument in motion.

Refinancing a 5% Mortgage Fee to a 3% Fee

$500k mortgage quantity @5% = $2,684.11

$500k mortgage quantity @3% = $2,108.02

Month-to-month financial savings: $576

Bear in mind these 3% mortgage charges that have been obtainable in 2021? Effectively, a number of owners with higher-rate mortgages took benefit.

Many have been in a position to scale back their price from 5% to three%, saving lots of per 30 days within the course of.

Utilizing our identical $500,000 mortgage quantity, the month-to-month P&I’d drop from $2,684.11 to $2,108.02.

That’d signify a month-to-month financial savings of $576. Whereas nonetheless an enormous discount in cost, it’s about $100 lower than the prior state of affairs of going from an 8% mortgage price to a 6% mortgage price.

Because of this I don’t subscribe to a sure refinance rule of thumb, such because the 1% rule or another mounted quantity.

There are numerous eventualities, and what works for one borrower could not work for an additional.

As you may see, it’s simpler to economize when refinancing a high-rate mortgage than it’s a low-rate mortgage.

Merely put, there’s extra room to save lots of if your house mortgage has the next rate of interest.

Conversely, if you have already got a low-rate mortgage, the financial savings are diminished as a result of your curiosity expense is small to start with.

What this implies is as mortgage charges enhance, debtors with high-rate loans will discover themselves “within the cash” for a refinance extra simply.

In any case, if it can save you more cash every month, offsetting any upfront prices related to the refinance shall be much less of a job. You’ll have the ability to break even faster.

And also you’ll take pleasure in extra cost aid.

Lastly, your total curiosity financial savings shall be higher. We’re speaking $242,000 in financial savings going from 8% to six% versus $207,000 when going from 5% to three%.

Whole curiosity paid throughout 30-year mortgage time period:

3% price: $258,887.20

4% price: $359,348.80

5% price: $466,279.60

6% price: $579,190.00

7% price: $697,543.60

8% price: $820,775.20

Learn extra: How does mortgage refinancing work?